#120 - Interest

Unprecedented, consequences, and coming to terms

This one’s on interest rates.

I won’t hold it against you if you stop reading here. See you next week if so.

For those remaining… Strap yourselves in.

Welcome! If you’re reading this but haven’t subscribed you can do here:

Unprecedented

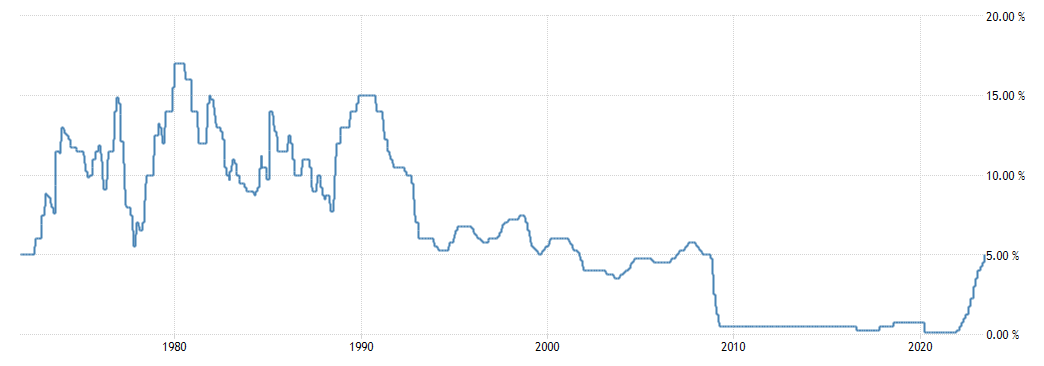

Interest rates are in the news.

They’re on a meteoric rise.

Just 18 months ago the Bank of England base rate sat at 0.25%. Off the back of 14 years(!) below 1%.

Those numbers are long gone. We’re now at 5% with every chance of going higher.

So what? Does it matter?

Yes, it turns out. Yes it does.

Before we go into all that, there’s one point to highlight: This is far from unprecedented.

What was unprecedented was the 14 years of sub 1%. Here’s the above graph zoomed out:

The 40 years prior barely dipped below 5%. If anything we’re getting back to the norm.

But that doesn’t mean we’re out the woods. Far from it.

Consequences

Because everything is relative.

It doesn’t really matter what interest rates were in the 90s. What matters is interest rates when we took out our mortgage, or launched our business.

For millions these decisions were made in a period of rock bottom rates. Free money. 5%+ rates were thought an impossibility.

Deals were signed, plans were made, and dies were cast. Now the consequences.

One such consequence is for tens of thousands of mortgage holders. They’ll see repayments rocket as they move from fixed rate to variable. We’re talking hundreds or thousands of pounds more a month for people already struggling to make ends meet.

For many the only option will be to sell.

This in turn will flood the property market with desperate sellers. A market with demand already hit by more expensive mortgages. You see the problem.

Coming to Terms

A similar dynamic is playing out in startups. The last decade was built on promises of unlimited capital. That’s come crashing down to earth. There’s a lot less money out there.

The hardest thing is coming to terms with that.

That what worked, or looked like it might, is just not viable anymore. The writing is well and truly on the wall, whether we’re looking or not.

There’s a wonderful story from Only the Paranoid Survive by Andy Grove of Intel. At the time Intel’s core memory business was getting hammered by competitors in a race to the bottom. The below is his conversation with the CEO, Gordon Moore:

"If we got kicked out and the board brought in a new CEO, what do you think he would do?"

Gordon answered without hesitation, "He would get us out of memories."

I stared at him, numb, then said, "Why shouldn't you and I walk out the door, come back and do it ourselves?"

They did exactly that.

It saved the company and the rest, as they say, is history.

Whether it’s mortgages or startup funding, we’re no doubt in for a choppy time ahead. But, as ever, there’s hope. Face the reality of your particular situation and there’s always a way through.

Just note that everything has changed. It’s time to face that. Time to learn the new rules. The new game. And figure out the new path forward.

And once you have that? Walk out the door, come back and do it yourself. Make it happen.

Do that and the world is your oyster. Good luck.

My Week in Books📚

Replay by Ken Grimwood

If you lived 20 years over and over again, what would you do differently? A wonderful book. Thought provoking.

Thank you Jack Smith for the rec!

Psychology of Money by Morgan Housel

Basically 20 blog posts published in a book but a good read. MH has a unique and incredibly perceptive view of our relationship with money. Much more subjective than we think.

Book recommendations welcome & encouraged. Just hit reply! 🙏

Unplugged 🌳📵

From the blog: Unplugging Post-Digital Detox

A Final Thought 💡

“Truth is like the sun. You can shut it out for a time, but it ain’t goin’ away.”

—Elvis Presley

— —

P.S. The "♡ Like" button looks insignificant, but it indicates Unplugging’s worth to visitors. Please don't hesitate to show your support. Thank you!

Fascinating how this will play out. I’m glad we’re out of the pegged interest rate era as it wasn’t sustainable.